The Independent Uganda: You get the Truth we Pay the Price

The Independent Uganda: You get the Truth we Pay the Price

Earlier, the director for commercial banking at the BoU Benedict Sekabira told The EastAfrican that financial institutions had finalised on the compliance requirements but were facing challenges in obtaining reliable data on credit transactions.

Sekabira said data on small and medium-size enterprises (SMEs) — the largest pool of borrowers — was only available for two years whereas data covering 20 years of inflation, economic growth rates, exchange rates and clients’ credit history was required.

However in Kenya, guidelines issued by the Central Bank (CBK) last December allowed banks a five year transition period during which expected losses charged on income should be recouped to avoid eroding the banks’ core capital. It also proposed CBK provisions above the IFRS 9 requirements be charged on reserves instead of on income.

“During the transition period, institutions should disclose in their published results their core and total capital ratios both before and after the additional expected credit loss provisions have been added back,” the bank said.

What next?

Going forward, Kibbedi said financial institutions will be required to train their staff to ensure that they do not simply lend out cash but also follow up their clients as well as their activities for purposes of loan recovery.

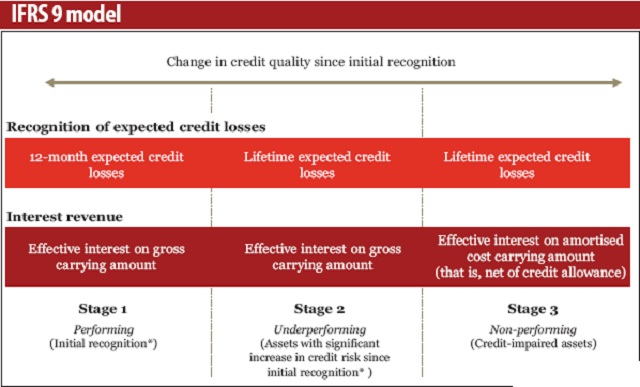

How loans will be will be classified under the IFRS 9

Under the IFRS 9, loans and credit will be classified in three ‘stages’ – performing, underperforming and impaired. When a loan is made, which is stage one, the lender must make provision equivalent to the expected loss on it over 12 months.

If the credit risk increases but the loan is still good, it moves to stage two, and it is where the lender has to increase the provision to the expected loss over the life of the loan.

If the loan goes bad, it passes to stage three, with the provision similar to those of stage two, but from then on the bank books less interest revenue in proportion to the expected loss on the loan.

Infact the new IFRS9 standard is bound to affect agricultural credit provision to farmers since they are the dorminant popn segment with low household income ,so the increased cost of borrowing will scare away a big number of agricultural clients with in the country